Buy-to-let Investment Property Guide

Buying a property as a buy-to-let investment should be considered a medium to long-term investment, ideal for those who prefer to invest in a tangible asset unlike stocks and shares. Buy-to-let property investors main focus is to achieve the highest possible yield and currently most yields offer a better return than banks and building societies particularly when you factor in potential for capital growth. The percentage yield only takes into account the rental income, it does not consider the advantages of capital growth as the value of a property can increase during a longer period of investment.

The following short guide is designed to give you a quick and simple summary on buying-to let as an investment.

1. What is Buy-to-let?

Buy-to-let is a property investment strategy whereby a property is purchased with the intention to rent it out for profit. As the owner of the property, you can benefit from any increases in the property value, meanwhile any rental income can be used to meet the loan repayments if there is a mortgage on the property, otherwise the income is profit.

When you buy a property, you become a landlord and you are required to understand your responsibilities and duties to your tenant. For peace of mind as a landlord, use our property management services - we can take care of all aspects of letting your property.

2. Let us know you are looking

The first step to finding the right buy-to-let investment property is to let us know you are looking. Contact your nearest Frost office or register your property requirements with us. It may take a while to find the right investment property - sign up for property alerts and receive updates when properties you are interested in become available.

3. Which areas would you consider buying in?

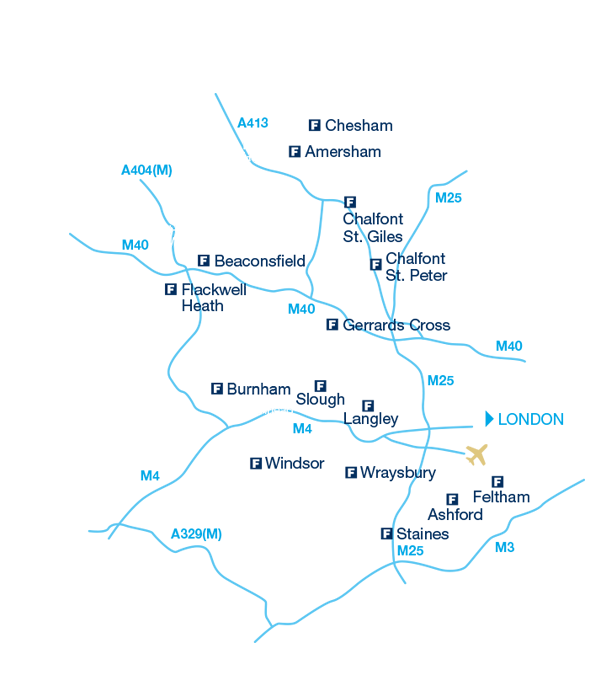

Research your area. Getting to know the area in which you wish to purchase your buy-to-let property is vitally important. Schools, shops and transport links will appeal to tenants. All the areas we cover offer excellent transport links via railways and the motorway network including the M25, M4 and M40 - ideal for commuting to London and Heathrow airport.

4. Finding a buy-to-let investment property

- View our residential properties for sale

- View our commercial properties for sale

- View our New Homes for sale

- View our investment properties

- Discover more about the areas we cover

Residential property search Search our residential sales database by:

Prepare - read our guides

Residential: Buying guide, letting guide, renting guide, selling guide.

Commercial: Buying guide, letting guide, renting guide, selling guide

Speak to one of our commercial agents or contact your nearest Frost office to find out about the latest investment opportunities.

5. What type of property makes a good buy-to-let investment?

The type of property you invest in will dictate the type of tenants it attracts and how much time or additional finances your property will take for you to manage it.

Residential Investment properties

Residential properties range from land with development potential, flats, houses and estates. While some investors like to renovate a property or they are attracted to the unique character of older style properties, other investors prefer brand New Homes with less maintenance issues.

View our investment properties

Commercial Investment properties

Commercial property can be a more rewarding investment due to their lease terms averaging 3-5+ years, enabling you to have a more secure return on your investment.

Commercial properties range from land with development potential, office space, retail outlets, and industrial units in varying locations such as industrial estates, high street, town centres or business parks. Contact our commercial team.

6. Financing your investment property

The two most important aspects of an investment property are that it financially works for you and that the property appeals to the right tenants to maximise a good rental yield.

- Mortgage advice

We work with reputable, trusted independent mortgage advisors who carefully assess your circumstances and help you find your target property price and help you get the best possible buy-to-let mortgage. - Buy-to-let mortgages

Generally these require a deposit of 15-25% of the property’s market value and the mortgage lender will base your mortgage off the investment potential of your property not your salary. - Re-mortgage / release equity

Have you thought about releasing equity in your other existing properties to fund a new purchase? Arrange a valuation of your property, or speak to our independent mortgage advisors to determine the right mortgage for you.

7. What costs are involved with purchasing a property?

The biggest cost of a buy-to-let investment is usually the mortgage repayment fee, however other costs associated with buying a property include:

- Buying the property

- Property maintenance

- Mortgage fees

- Application fee

- Survey fees

- Solicitor fees

- Stamp duty

- Buildings insurance

Learn more, read our residential buying guide, commercial buying guide.

8. Landlord's responsibilities

Subject to the terms of contract, landlords are usually responsible for most repairs to the property’s structure and exterior, heating and water systems, installations / fittings, safety of gas appliances and generally ensuring the electrics are safe. Being a landlord can be demanding - if you lead a busy life and you are unable to provide the attention your property and tenants need, then consider property management.

Our property management services include:

- Finding tenants

- Obtaining tenant references

- Collecting rent from tenants

- Maintaining the condition of the property

- Resolving any problems that may arise

- Meeting the fire safety requirements for furniture/furnishings

For many investors property management services simply ensure everything runs smoothly from property to tenant and from paperwork to maintenance work. Read what our clients say.